Valuer Insights

Business Insights | Pay for What You Build

Understanding Hong Kong's New Land Premium Policy

July 3, 2026

Contact

Senior Director, Valuation & Advisory Services, Hong Kong

The “Pay for What you Build” Scheme

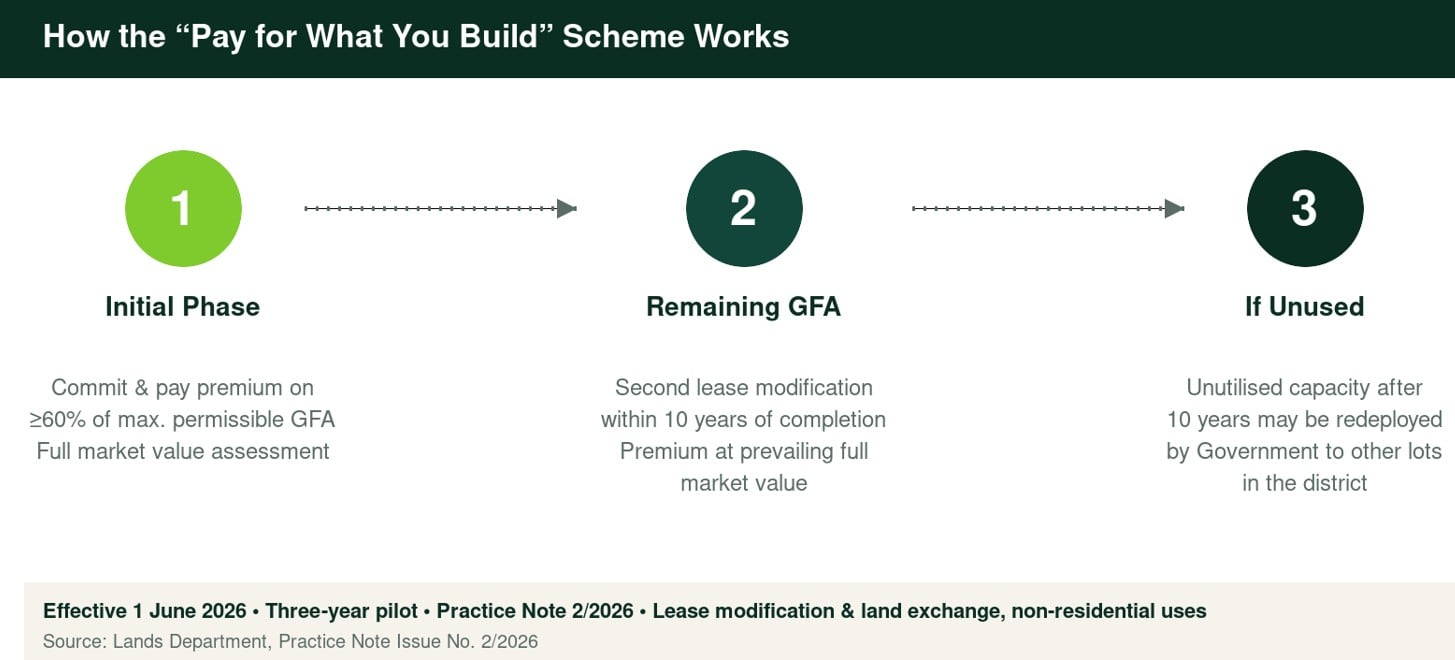

The Lands Department has introduced a three year pilot scheme on “Pay for What You Build” (the “Scheme’) under Practice Note Issue No. 2/2026, effective from 1 June 2026. The Scheme is applicable to all lease modification and land exchange applications for non-residential developments throughout the territory. Applicants are required to undertake an Initial Phase Development (the “Initial Phase”) comprising no less than 60% of the total permissible maximum gross floor area (“GFA”) of the whole development, to be completed in time in accordance with the building covenant. The land premium is assessed based on the full market value of the GFA attributable to the Initial Phase and the "preferred use" of the land proposed by the lot owners.The remaining development potential may be realised through another lease modification within 10 years following completion of the Initial Phase, with premiums assessed at prevailing full market value. Any unutilised development capacity upon expiry of the 10-year period may be redeployed by the Government to other lots in the district.

The Northern Metropolis and Policy Intent

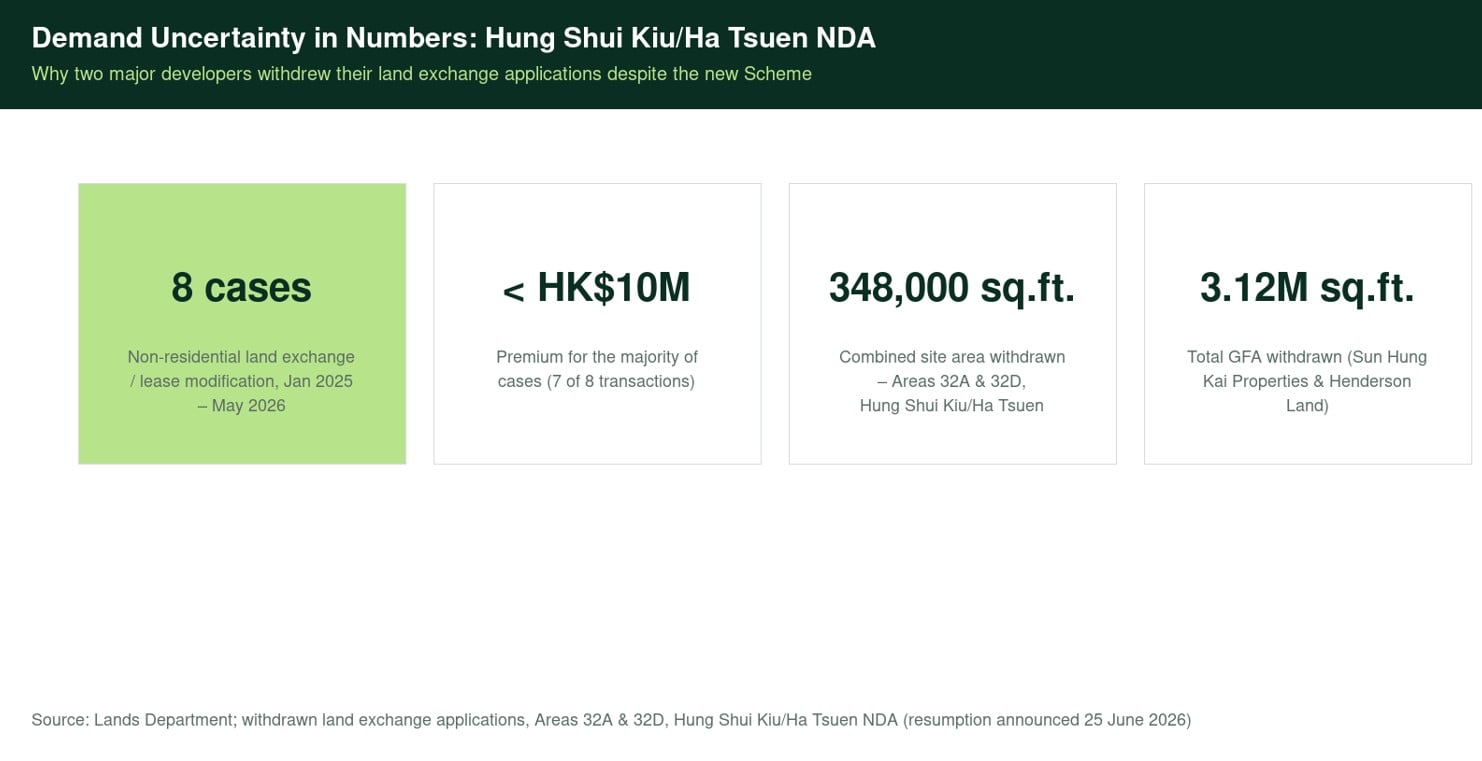

As highlighted in the 2025 Policy Address, the Scheme is linked to the development of the Northern Metropolis, which places strong emphasis on technology, industry and education. Unlike established urban districts, many planned economic clusters in the Northern Metropolis, particularly industrial and innovation and technology (“I&T”) hubs such as the San Tin Technopole, are characterised by uncertain and evolving occupier demand. This is further compounded by high vacancy rates and substantial new office supply in urban areas, where it is anticipated that multiple years will be required to absorb excess office space, particularly in non-core locations. Collectively, these factors heighten investment risk and capital outlays, giving rise to a structural challenge whereby revenue realisation in the Northern Metropolis is inherently uncertain.Demand uncertainty is further evidenced by the limited number of land exchange and lease modification cases for non-residential uses1. According to data published by the Lands Department, only 8 such cases, excluding modifications of a technical nature involving nil premium, were executed between January 2025 and May 2026. Notably, the majority of cases were small-scale developments, with land premiums below HK$10,000,000 2, indicating a cautious investment stance among developers and limited appetite for large-scale non-residential projects.

Under the conventional land premium assessment mechanism, premiums are determined based on the permissible maximum GFA of the lot and the use having the highest market value as assumed by the Lands Department. This approach implicitly assumes full and immediate development potential. While appropriate in mature markets, it may overstate the value in emerging districts where tenant demand is untested and likely to materialise progressively over an extended period.

The resulting mismatch between substantial upfront premium payments and deferred or uncertain income streams places considerable financial strain on developers and investors. High financing costs further exacerbate this imbalance, raising gearing levels and overall project risk. Consequently, developers and investors may defer investment decisions or limit participation.

Against this backdrop, the policy intent of the Scheme is to recalibrate the risk-sharing framework between the Government and developers. By allowing deferral of a portion of land premium payments, the Scheme reduces initial capital outlays and alleviates financing pressures by reducing borrowing needs and associated interest expenses.

Importantly, the scheme facilitates a phased development approach, allowing developers to align construction with actual market demand. This provides flexibility to test tenant uptake before committing to full build out, thereby mitigating demand uncertainty intrinsic to new economic zones in its early development stage. Developers may also retain the option not to proceed with the remaining development if market conditions remain weak, avoiding over commitment of capital and penalty for breach of the building covenant under lease. Collectively, these features are intended to incentivise earlier project commencement and enhance market responsiveness in the Northern Metropolis.

Comparative Case Study – URA Option Scheme in Singapore

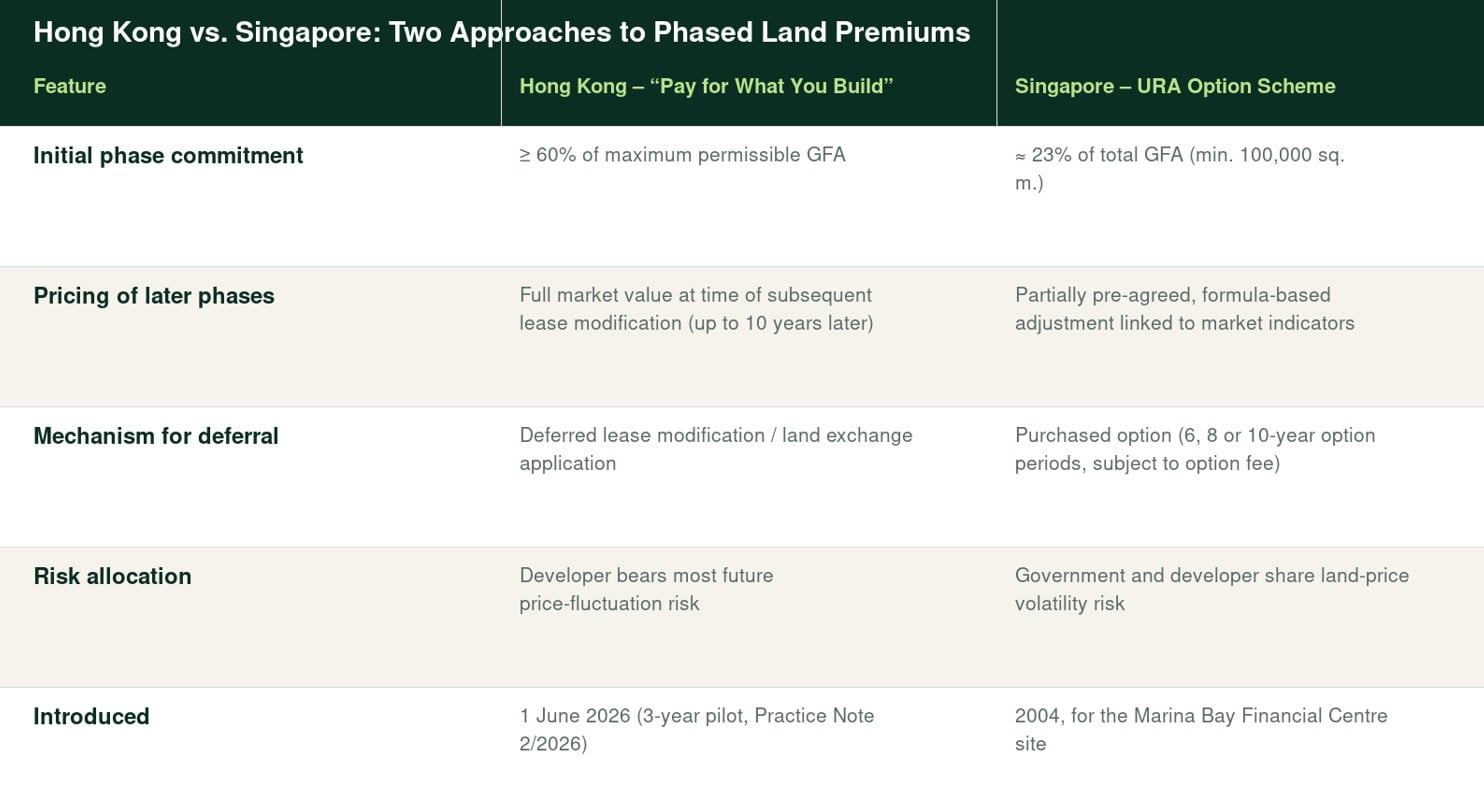

A comparable reference case for addressing large scale, high uncertainty developments is Singapore’s “option scheme” launched by the Urban Redevelopment Authority (“URA”). It was first introduced in 2004 for the Marina Bay Financial Centre (“MBFC”) site. The MBFC site represented a complex and capital intensive project, yielding approximately 438,000 sq. m. of GFA within a mixed use, infrastructure integrated development 3. As a reclaimed site positioned as a future extension of the traditional Central Business District, it was subject to uncertain tenant demand and cyclical office market conditions following the Asian Financial Crisis.Under the option scheme, the developer was required to commit to and pay for an initial phase of development upfront, comprising at least 100,000 sq. m. of GFA, which is approximately 23% of the total GFA. The developer will purchase an option for the right to acquire subsequent phases at prices fixed by a formula linked partly to market indicators based on the tender bid for the initial phase 4. The developer has a choice of option periods of 6, 8 and 10 years, subject to the payment of corresponding option fees 5.

This framework shares conceptual similarities with the “Pay for What You Build” approach. Both schemes seek to address demand uncertainty and high upfront capital requirements by facilitating phased development and deferring financial commitments. In both cases, the Government shares part of the market risk, enabling developers to align investment more closely with actual demand, thereby improving project viability and encouraging participation in strategic but unproven locations. The Singapore scheme has been widely regarded as successful. It attracted consortium bidders despite the site’s scale and risk profile. The development played a catalytic role in establishing Marina Bay as a major extension of Singapore’s CBD.

A key difference, however, lies in the treatment of future land pricing. While the currently implemented Hong Kong Scheme defers premium payment for later phases based on prevailing market conditions at the time of subsequent lease modification, the Singapore model provides a partially pre agreed pricing mechanism through its formula based adjustment. This will provide the developer with some certainty in the price for the subsequent phases and allow the Government and the developer to share the risk of land price volatility. By contrast, the Hong Kong approach places greater exposure on developers to future price fluctuations.

Policy Considerations and Conclusion

Notwithstanding the merits of the “Pay for What You Build” framework, market participation may remain measured in the near term, given continued uncertainty in tenant demand within the Northern Metropolis. While the Scheme introduces a mechanism to defer part of the land premium based on the extent of development undertaken, its effectiveness is inherently shaped by two structural constraints.First, the requirement for developers to commit to a minimum of 60% of the maximum permissible GFA substantially weakens the extent of phased development. In typical urban redevelopment scenarios, where sites are relatively small and projects are often undertaken in a single phase, this threshold necessitates a near full-scale upfront commitment. Consequently, the Scheme offers only marginal relief in terms of cash flow timing, rather than a fundamental shift in development risk. Moreover, as urban sites generally involve lower absolute capital exposure and more observable market demand, there is limited incentive to utilise the Scheme in such contexts, notwithstanding its citywide applicability.

In contrast, large-scale sites within New Development Areas (“NDAs”) are characterised by significant upfront investment, longer absorption horizons, and heightened demand uncertainty. The requirement to undertake at least 60% of total GFA in the Initial Phase remains substantial relative to demand, particularly in the context of large-scale land supply in the Northern Metropolis. A lower threshold, potentially 20% to 30% of total GFA for some designated areas in the Northern Metropolis, could better reflect development phasing needs and improve feasibility, particularly for large scale or infrastructure dependent projects.

Meanwhile, land within NDAs is now predominately supplied through government land sale programmes and developers have generally demonstrated a preference for ex-gratia compensation under land resumption by the government, rather than pursuing lease modifications or land exchanges. This raises questions about the practical applicability of the Scheme in these areas. This is underscored by the recent withdrawal of land exchange applications, despite the Scheme being in effect, by two major developers, Sun Hung Kai Properties and Henderson Land, in respect of their land holdings in Area 32A 6 and Area 32D 7 in Hung Shui Kiu/Ha Tsuen NDA. These sites, with a combined commercial site area of approximately 348,000 sq. ft. and total GFA of around 3.12 million sq. ft., were withdrawn. On 25 June 2026, the Lands Department announced the resumption involving these two sites of withdrawn in-situ land exchange applications. This suggests that landowners remain unconvinced by the newly implemented “Pay for What You Build” Pilot Scheme, with underlying market demand uncertainty continuing to be the primary consideration. Accordingly, the overall effectiveness of the Scheme remains open to question.

In addition, the use of conventional land premium assessment for subsequent phases exposes developers to future pricing uncertainty. The Singapore experience suggests that incorporating greater certainty over the land premium for the remaining GFA may enhance the attractiveness of the Scheme. A structured pricing mechanism, such as a formula based adjustment on centralised land price proxy, may provide clearer visibility over future land costs while retaining flexibility for market changes. Alternatively, freezing the land premium unit rate at the time of lease modification of the Initial Phase would further reduce development risk and improve investment attractiveness.

Taken together, the Scheme is likely to have a selective and case-specific impact, rather than serving as a broad-based catalyst for non-residential development. Its ability to influence developer behaviour will depend less on the deferral of land premiums per se, and more on whether it meaningfully addresses the underlying mismatch between development scale, market demand, and the timing of investment.

The article is authored in support of Paula Yuen, Manager, Valuation & Advisory Services, Hong Kong, and Edwin Lai, Valuer, Valuation & Advisory Services, Hong Kong with valuable research, content development, and editorial contributions.

1 Non-residential uses include commercial, hotel, industrial / godown uses, but exclude residential, institution / community and other uses.

2 7 of the land exchange and lease modification cases for non-residential uses involved land premiums ranging from HK$106,000 to HK$9,850,000, and a case of HK$150,000,000 for the lease modification at 57-61 Ta Chuen Ping Street in Kwai Chung.

3 The MBFC site was zoned ‘White”, with at least 60% of the GFA designated for office use, while the remainder could accommodate other commercial uses, as well as complementary hotel, residential, entertainment, and recreational uses.

4 For subsequent phases, the bid unit price will be adjusted for changes in market prices to compute the land price for exercising the option. The adjustment to the bid unit price will be 50% of the percentage change in the average Development Charge rates for commercial land use in the core Central Business District.

5 Option fees are 6%, 8% and 10% of the land price of the remaining phases for option periods of 6, 8 and 10 years respectively and 3% of the option fee percentage paid can be used to offset part of the land premium for purchases of the subsequent phases.

6 Area 32A in Hung Shui Kiu/Ha Tsuen NDA lies within an area zoned “Commercial (1)” under Draft Hung Shui Kiu and Ha Tsuen Outline Zoning Plan No. S/HSK/3 with a maximum plot ratio of 9.5 and maximum building height of 200mPD.

7 Area 32D in Hung Shui Kiu/Ha Tsuen NDA lies within an area zoned “Commercial (2)” under Draft Hung Shui Kiu and Ha Tsuen Outline Zoning Plan No. S/HSK/3 with a maximum plot ratio of 8 and maximum building height of 200mPD.

Reference:

Practice Note, Lands Administration Office, Lands Department

URA Releases the Business and Financial Centre (BFC) Site for Sale on Reserve List

Government posts fifth batch of land resumption notices for Second Phase development of Hung Shui Kiu/Ha Tsuen New Development Area and G.N. 3831