Valuer Insights

Business Insights | Rate Cut & Policy Relief: How Hong Kong Residential Market is Poised for a Recovery

September 30, 2025

Contact

Angus Luk

Senior Director, Valuation & Advisory Services, Hong Kong

Following the Federal Reserve's announcement of a 25-basis-point reduction in interest rates on September 18th, HSBC has responded by lowering its Hong Kong dollar Prime Rate from 5.25% to 5.125%, effective September 19th.

Consequently, with HSBC's capped mortgage interest rate set at P-1.75%, the effective interest rate on mortgages will decrease from 3.5% to 3.375%. This adjustment will result in a reduction of approximately HK$347 in monthly mortgage payments for a HK$5 million loan over a 30-year amortization period, lowering the monthly payment from HK$22,452 to HK$22,105.

Buyers of smaller residential units, often comprising young professionals and emerging families, typically allocate a larger percentage of their income towards mortgage repayments, rendering them highly sensitive to interest rate fluctuations. In contrast to luxury home purchasers, these buyers are generally more sensitive to cash flow considerations, thus amplifying the immediate financial relief offered by the rate cut.

Furthermore, sustained rental demand coupled with elevated rental prices, compounded by the rate cut, may incentivize tenants to transition into homeownership, leveraging the combined effect of rising rents and declining interest rates. The reduction in interest rates also diminishes the appeal of fixed deposits, potentially redirecting capital towards the residential market and bolstering buy-to-let investment activity.

This adjustment to the NCIES, lowering the investment threshold for residential properties, is anticipated to stimulate demand within the luxury residential segment, encompassing high-end apartments and detached houses. In 2024, a total of 1,491 transactions involving residential properties valued above HK$30 million were recorded, representing 21.7% of the total transaction value, or HK$103.73 billion, and accounting for 2.8% of the total transaction volume. Preliminary data for the first eight months of 2025 show 906 transactions in this category, accounting for 2.1% of total volume and HK$56.29 billion in aggregate value, a YoY decline of 17.6%. However, transaction activity in this segment is expected to pick up in the remaining months of 2025, driven by renewed investor interest following the NCIES enhancement.

As of the end of August 2025, the NCIES had received over 1,900 applications. The relaxation of real estate investment criteria is expected to further incentivize the allocation of capital towards the property sector.

Driven by the gradual strengthening of both primary and secondary market transactions, coupled with the supportive measures outlined in the Policy Address and the recent interest rate cut, new developments are poised to be the primary beneficiaries. Based on preliminary data for the first eight months of 2025, the primary market recorded 12,962 transactions, resulting in an average monthly volume of 1,620 units. Consequently, the forecast for the full-year primary sales volume is expected to exceed 19,000 units, reflecting a potential year-on-year increase of over 15%. Furthermore, should developers accelerate the launch of new projects and proactively manage existing inventory before the end of the year, the market may potentially approach the 20,000-unit threshold. The current inventory of new properties primarily comprises medium-sized units, catering to the needs of first-time homebuyers. The reduction in interest rates is expected to further reduce overall acquisition costs for buyers, thereby stimulating sales within new developments, particularly in the New Territories and Kowloon, where a higher concentration of smaller units is available.

Regarding the secondary residential market, based on transaction data from the first eight months of 2025, a total of 29,417 transactions were recorded, resulting in an average monthly volume of 3,677 units. Projections for the full-year transaction volume anticipate exceeding 44,000 units, representing a year-on-year increase of over 8% and reaching a four-year high.

As consensus builds that rates have peaked and are trending downward, buyers perceive less risk of further price corrections. Recovery typically follows a “volume leads price” pattern, where transaction activity strengthens first—driven by lower homeownership costs and renewed confidence—before price growth gradually follows. This will manifest as a notable increase in transaction activity across both primary and secondary markets, particularly in areas with a high concentration of new developments, such as Yuen Long, Tuen Mun, and Kai Tak in Kowloon East.

Subsequently, increasing transaction volumes will facilitate the absorption of lower-priced properties, thereby contributing to the stabilization of residential prices. As existing homeowners experience reduced holding pressure, their negotiating margins will contract, leading to a stabilization of the price decline and the commencement of a consolidation phase. Finally, residential property prices are poised to regain upward momentum. Continued interest rate cuts, coupled with favorable local economic conditions, will provide robust support for residential prices and are expected to propel them back onto an upward growth trajectory.

Consequently, with HSBC's capped mortgage interest rate set at P-1.75%, the effective interest rate on mortgages will decrease from 3.5% to 3.375%. This adjustment will result in a reduction of approximately HK$347 in monthly mortgage payments for a HK$5 million loan over a 30-year amortization period, lowering the monthly payment from HK$22,452 to HK$22,105.

Rate Cuts Spark Surge in Home Buying for Rental Yields

While the magnitude of the rate cut is modest, its impact is anticipated to be more pronounced within the Hong Kong residential market, particularly for new developments targeting the smaller and medium-sized segments, relative to the luxury housing sector. The rate cut directly translates to a reduction in monthly mortgage obligations, offering the most significant benefit to younger prospective homebuyers with comparatively lower income levels.Buyers of smaller residential units, often comprising young professionals and emerging families, typically allocate a larger percentage of their income towards mortgage repayments, rendering them highly sensitive to interest rate fluctuations. In contrast to luxury home purchasers, these buyers are generally more sensitive to cash flow considerations, thus amplifying the immediate financial relief offered by the rate cut.

Furthermore, sustained rental demand coupled with elevated rental prices, compounded by the rate cut, may incentivize tenants to transition into homeownership, leveraging the combined effect of rising rents and declining interest rates. The reduction in interest rates also diminishes the appeal of fixed deposits, potentially redirecting capital towards the residential market and bolstering buy-to-let investment activity.

Policy Address Supports Residential Property Market

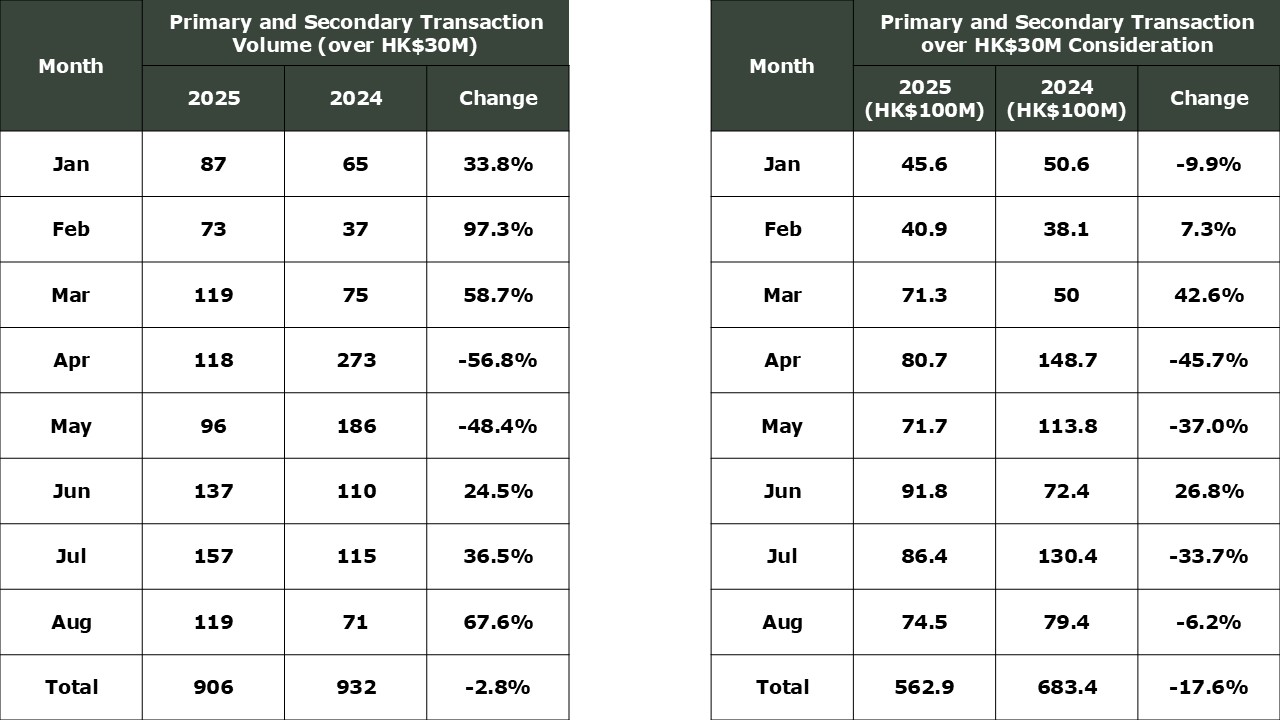

The recent Policy Address included a revision of the New Capital Investment Entrant Scheme (NCIES), specifically reducing the threshold of transaction price of residential real estate is reduced from HK$50 million to HK$30 million for one single property. The aggregate investment cap for the total investment amount in real estate which is counted towards the fulfillment of minimum investment threshold is raised from HK$10 million to HK$15 million (among which the cap on residential real estate remains at HK$10 million).This adjustment to the NCIES, lowering the investment threshold for residential properties, is anticipated to stimulate demand within the luxury residential segment, encompassing high-end apartments and detached houses. In 2024, a total of 1,491 transactions involving residential properties valued above HK$30 million were recorded, representing 21.7% of the total transaction value, or HK$103.73 billion, and accounting for 2.8% of the total transaction volume. Preliminary data for the first eight months of 2025 show 906 transactions in this category, accounting for 2.1% of total volume and HK$56.29 billion in aggregate value, a YoY decline of 17.6%. However, transaction activity in this segment is expected to pick up in the remaining months of 2025, driven by renewed investor interest following the NCIES enhancement.

Source: Land Registry

As of the end of August 2025, the NCIES had received over 1,900 applications. The relaxation of real estate investment criteria is expected to further incentivize the allocation of capital towards the property sector.

Improving Investment Market Facilities Residential Market Recovery

While the residential property market has demonstrated signs of bottoming out, the pace of price appreciation has been moderate. Despite this, Hong Kong property valuations remain comparatively low. The Hong Kong stock market has experienced a significant surge, with Hang Seng Index climbing from 18,000 to 27,000 points, representing a gain of nearly 50%, and gold prices have also reached record highs. In contrast, residential property prices in Hong Kong are still near a nine-year low. The robust performance has contributed to a recent recovery in property transaction activity.Driven by the gradual strengthening of both primary and secondary market transactions, coupled with the supportive measures outlined in the Policy Address and the recent interest rate cut, new developments are poised to be the primary beneficiaries. Based on preliminary data for the first eight months of 2025, the primary market recorded 12,962 transactions, resulting in an average monthly volume of 1,620 units. Consequently, the forecast for the full-year primary sales volume is expected to exceed 19,000 units, reflecting a potential year-on-year increase of over 15%. Furthermore, should developers accelerate the launch of new projects and proactively manage existing inventory before the end of the year, the market may potentially approach the 20,000-unit threshold. The current inventory of new properties primarily comprises medium-sized units, catering to the needs of first-time homebuyers. The reduction in interest rates is expected to further reduce overall acquisition costs for buyers, thereby stimulating sales within new developments, particularly in the New Territories and Kowloon, where a higher concentration of smaller units is available.

Source: Land Registry

Regarding the secondary residential market, based on transaction data from the first eight months of 2025, a total of 29,417 transactions were recorded, resulting in an average monthly volume of 3,677 units. Projections for the full-year transaction volume anticipate exceeding 44,000 units, representing a year-on-year increase of over 8% and reaching a four-year high.

Source: Land Registry

Residential Market Follows Volume-to-Price Transmission

The residential property market is highly sensitive to investor confidence and market expectations, with interest rate cuts acting as a powerful catalyst for sentiment shifts. The start of a rate-cutting cycle can transform a pessimistic outlook into one of gradual optimism, boosting buyer confidence and encouraging market participation.As consensus builds that rates have peaked and are trending downward, buyers perceive less risk of further price corrections. Recovery typically follows a “volume leads price” pattern, where transaction activity strengthens first—driven by lower homeownership costs and renewed confidence—before price growth gradually follows. This will manifest as a notable increase in transaction activity across both primary and secondary markets, particularly in areas with a high concentration of new developments, such as Yuen Long, Tuen Mun, and Kai Tak in Kowloon East.

Subsequently, increasing transaction volumes will facilitate the absorption of lower-priced properties, thereby contributing to the stabilization of residential prices. As existing homeowners experience reduced holding pressure, their negotiating margins will contract, leading to a stabilization of the price decline and the commencement of a consolidation phase. Finally, residential property prices are poised to regain upward momentum. Continued interest rate cuts, coupled with favorable local economic conditions, will provide robust support for residential prices and are expected to propel them back onto an upward growth trajectory.