Valuer Insights

Business Insights |Northern Metropolis: Hung Shui Kiu Large-Scale Land Disposal

Why the Market Has Spoken and What Comes Next

July 10, 2026

Contact

Why Bidder Participation Was Constrained

The E&T Operator Gap

The most fundamental challenge is the absence of credible Enterprise & Technology Park (E&T) operators willing to commit to the scale, duration and complexity demanded by this tender. The mandatory threshold requirement, every bidder must develop and operate at least HSKTL 19 (10,190 sq.m. site area & 50,950 sq. m. maximum GFA), means industrial participation is a non-negotiable precondition. Yet residential developers, who form the natural bid universe, cannot identify E&T partners with the track record, financial standing and long-term operational commitment that the Government's technical scoring demands. Without a credible anchor E&T operator, no consortium can produce a technically competitive proposal. This is not a pricing problem. It is a structural readiness problem — and one the Government's current tender design does nothing to resolve.Commercial Feasibility

The three E&T sites collectively span over 55,000 sq.m. of land area with a combined minimum GFA of approximately 165,000 sq.m., comparable in scale to a standalone industrial campus. These sites will generate prolonged negative cashflow as construction and fit-out costs are incurred years before any meaningful rental income materialises. With estimated total residential construction costs exceeding HK$15 billion across all sites over the 7-year building covenant period, the net profit attributable to the three residential sites, approximately 5,500 units and ~275,000 sq.m. GFA, becomes marginal once E&T losses are absorbed.This comes against a challenging market backdrop. Hong Kong's warehouse vacancy rate hit a record high of 13.0% at end-2025, easing only modestly to 12.8% in Q1 2026, when new leasing volume rose 17.4% year-on-year to 682,800 sq.ft. (CBRE Hong Kong Industrial Figures Q1 2026). The risk-adjusted return, relative to the time (7+ years) and capital (HK$15bn+) committed, does not justify a bid from a commercially disciplined developer.

Regulatory Incoherence Across Government Departments

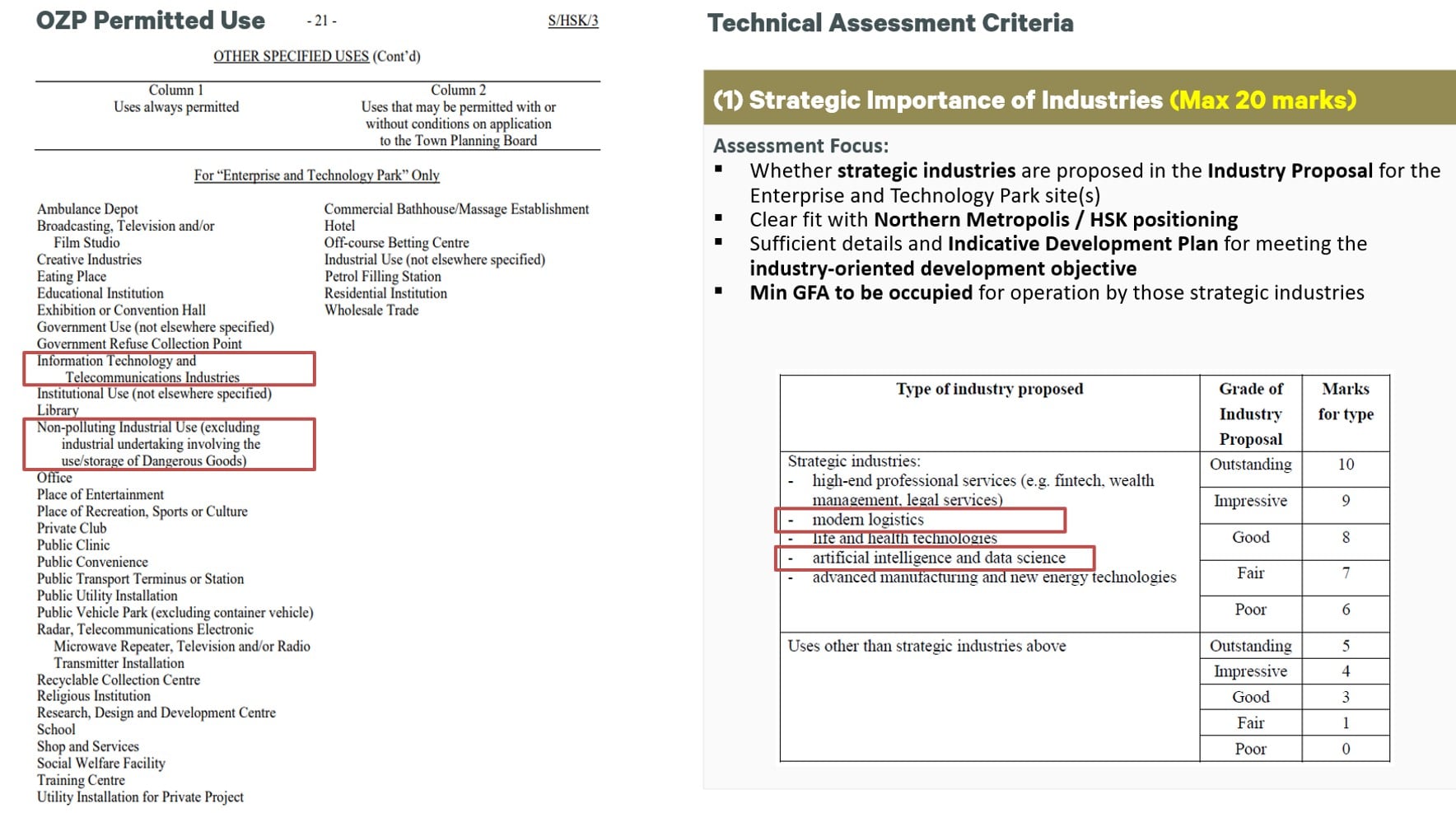

The non-premium technical proposal, worth 70% of the overall assessment, recommends advanced logistics as a high-scoring use for E&T sites. Yet the Government has confirmed in writing that pure warehouse use and 3PL logistics are not permitted under the OU (Enterprise & Technology Park) zone: "As there is no provision for 'Cargo Handling and Forwarding Facility' and 'Warehouse' uses in the Notes of the OU(E&TP) zone, pure warehouse use or 3PL operation is not permitted in this zone." Any logistics function must be ancillary to a qualifying industrial process to be considered at all. The scoring framework and the planning framework are telling developers two different things simultaneously.II to the Tender Notice “Strategic Industries”

Data centres present a parallel problem. The use is explicitly defined and permitted under the zoning. In practice, however, no government document confirms what power supply capacity, grid allocation or utility infrastructure is available for HSK/HT NDA at data centre scale — and power certainty is the primary site selection criterion for any serious data centre operator. A permitted use built on absent infrastructure commitments cannot attract credible bids.

Developers committing to a 50-year service deed cannot absorb regulatory ambiguity of this nature. Incoherence between the Planning Department's zoning, the Lands Department's lease conditions and the Development Bureau's scoring criteria is not a correctable footnote, it is a structural flaw in the tender design.

Disproportionate Liability Burden on the Consortium

Every E&T lot purchaser must enter into a service deed that remains effective throughout the 50-year land tenure, binding them to industry type, anchor enterprises, investment scale, employment targets and ongoing operational management. These are contractual obligations backed by bank bonds, capped at HK$10 million for HSKTL 19 and HK$20 million each for HSKTL 23 and 24, callable by the Government on written demand, unconditionally and immediately. The Purchaser must also submit regular progress reports and audited financial statements throughout the service period.Critically, premium payment liability is joint and several across all tendered lots under General Condition 2(c) of the Conditions of Sale. A residential developer in the consortium remains exposed to the full consolidated land premium — including for E&T sites — even where those sites are separately owned by another consortium entity. Where staged payment is elected, a single consolidated Premium Payment Guarantee must be submitted by a guarantor acceptable to the Government, further concentrating exposure. The service deed can in principle be novated upon assignment — but only with the Government's discretionary consent, on its own terms, with no automatic right of exit.

The result: a residential developer anchoring the bid carries joint and several premium liability across an industrial programme it does not operate, while having no direct means to control the operational performance that triggers the bank bonds and service deed enforcement. This liability architecture is structurally incompatible with how residential consortia manage risk — and it has not gone unnoticed in market engagement.

Physical and Locational Constraints on the E&T Sites

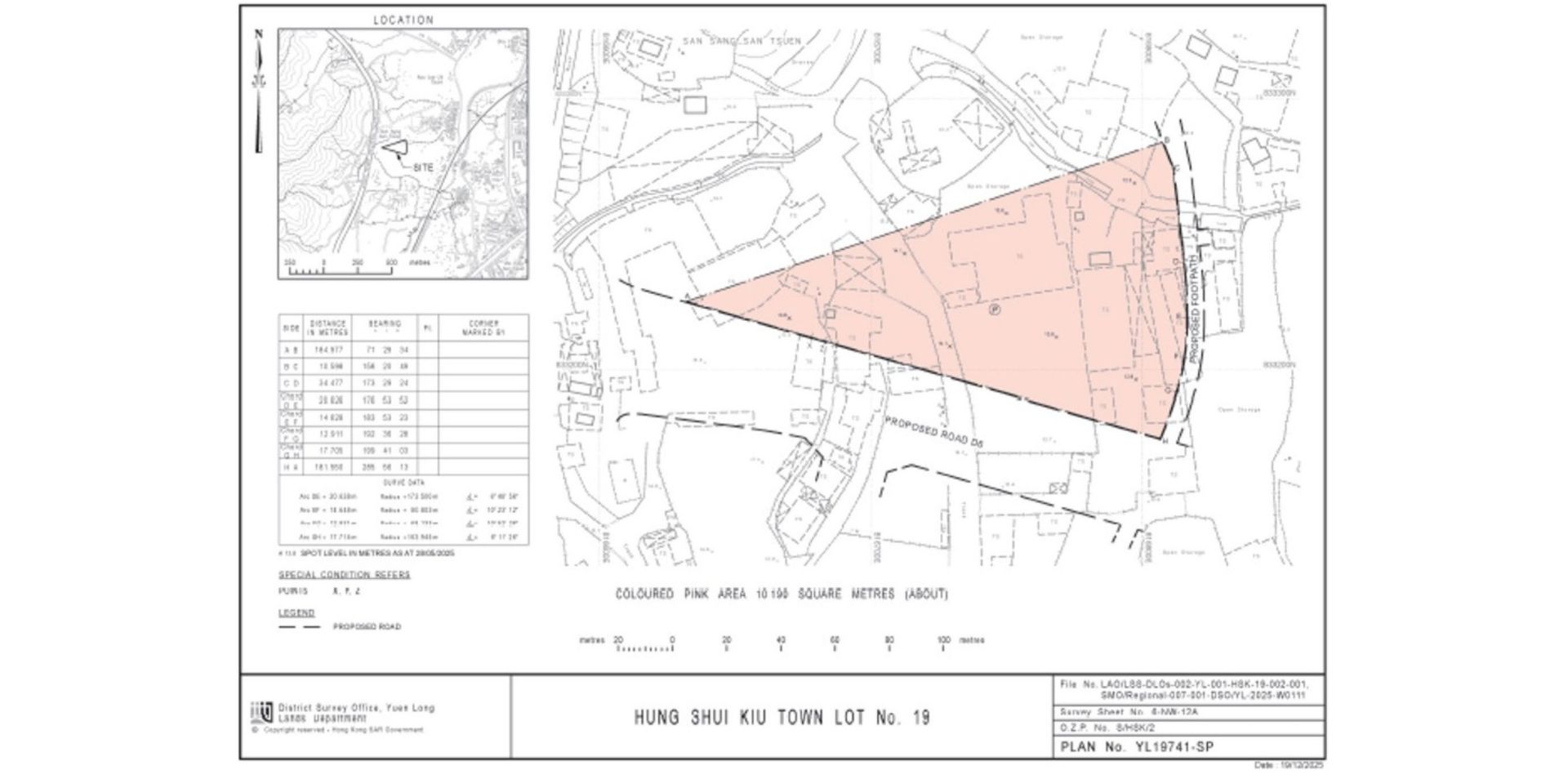

HSKTL 19 — the only site every bidder must include, is a triangular plot of 10,190 sq.m. Triangular floor plates are among the least efficient configurations for industrial occupiers, creating significant dead space and layout challenges for racking, loading and automation. The mandatory site carries the worst geometry in the package. What makes this particularly difficult to reconcile is that HSK/HT NDA is not a brownfield retrofit — it is a purpose-planned new city with a new road network designed from scratch. That the Government's own master planning process produced a triangularly shaped mandatory E&T site, in a development area where land parcels could theoretically have been drawn to any configuration, raises legitimate questions about how carefully site design was calibrated against actual industrial usability.

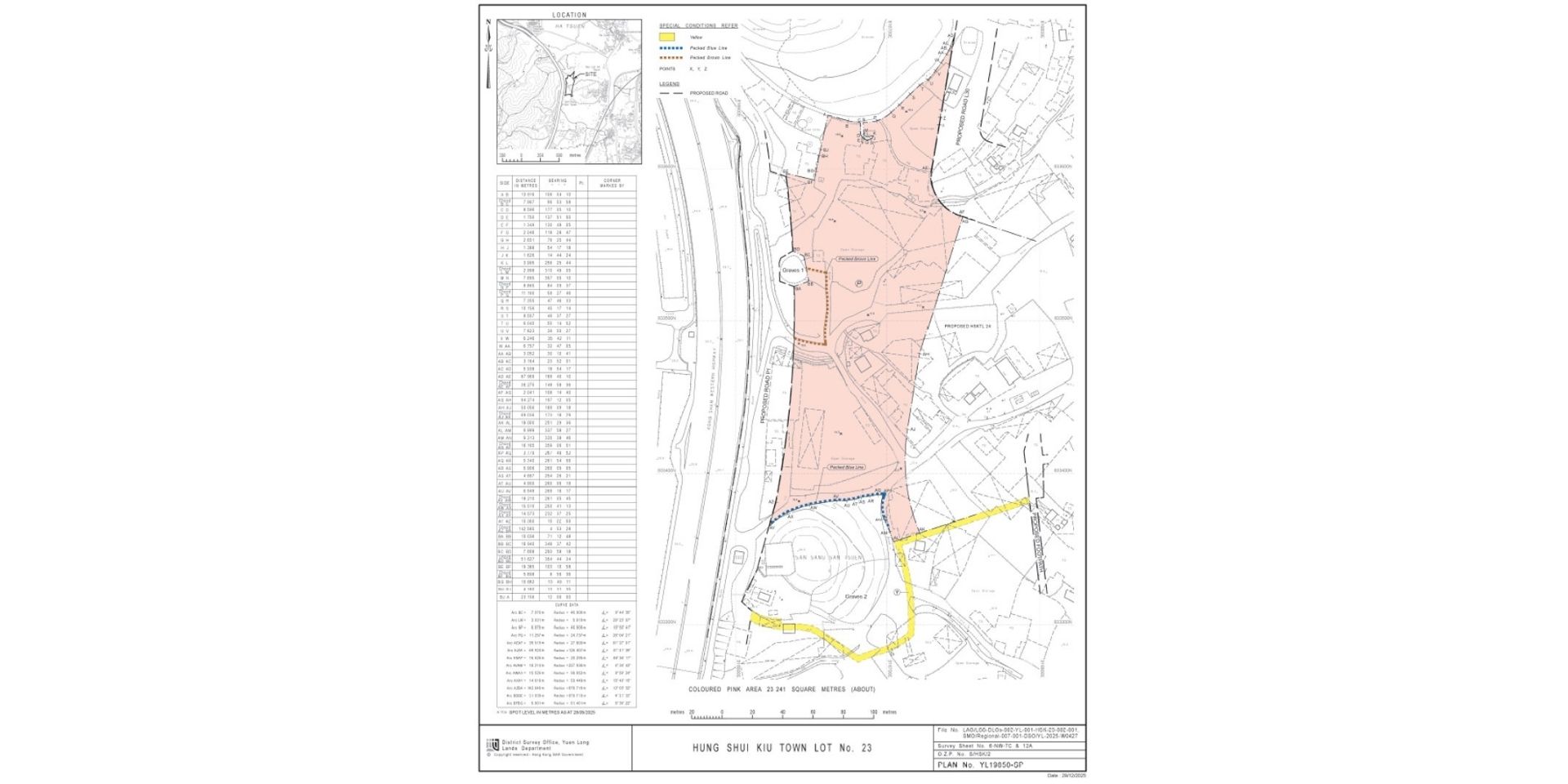

HSKTL 23 (23,241 sq.m.) carries an unusual encumbrance: the purchaser must provide permanent right-of-way for access to two existing graves on or adjacent to the site, including temporary footpath re-provision, until alternative access is completed. This directly affects ground-floor planning and site layout.

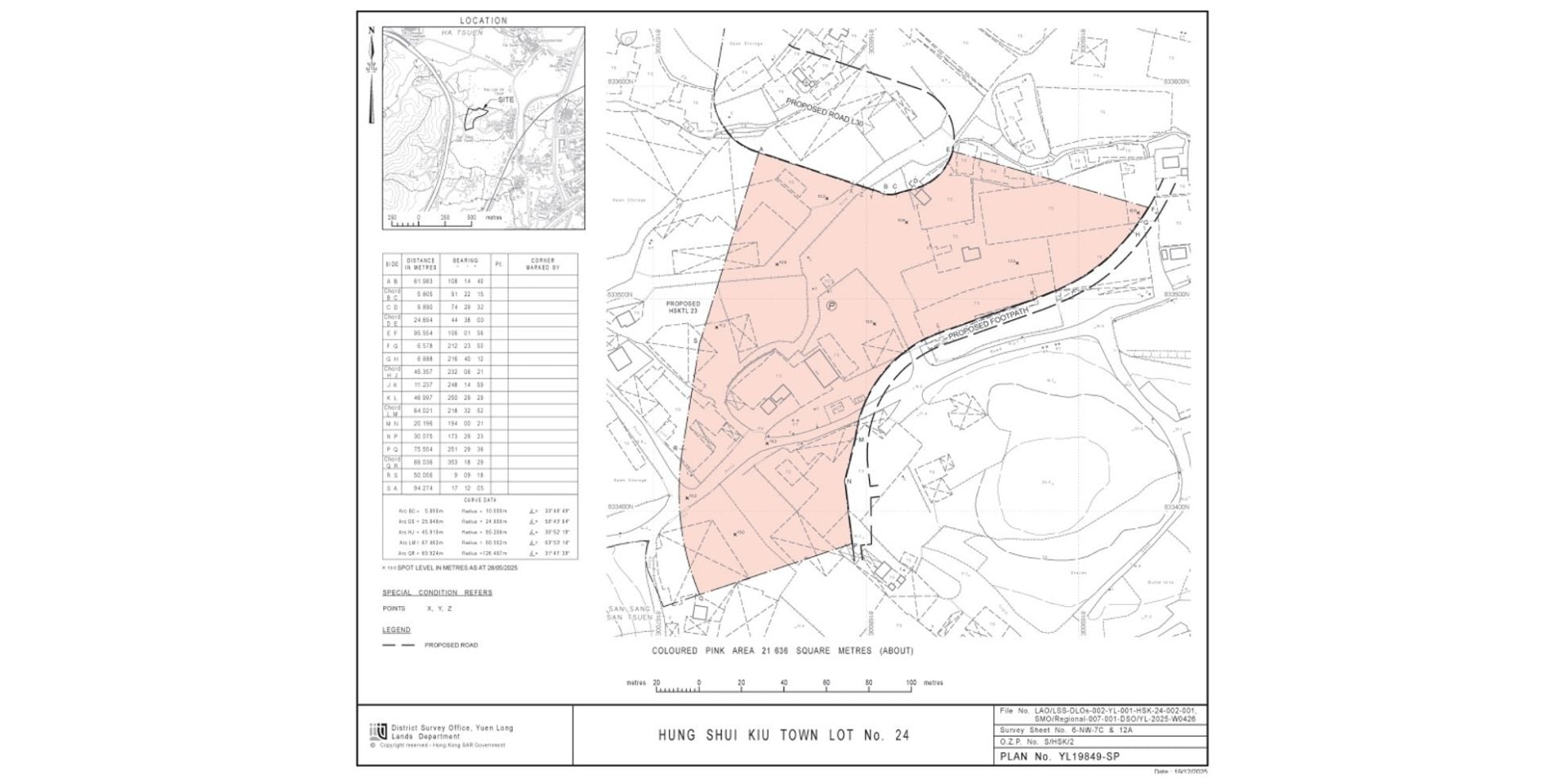

Figure 4: HSKTL No.24 Site Layout

HSKTL 24 (21,636 sq.m.) has an irregular, curved boundary, again constraining efficient floor plate design.

How the Government Should Reform LSLD for the 2027 Round

With two further LSLD sites expected in 2027, the Government has a narrow but real window to recalibrate. CBRE identifies four structural reforms.

-

Adopt Rolling Tenders

A six-month fixed tender window favours administrative convenience over strategic outcomes. A consortium committing over HK$15 billion and operating an E&T park for 50 years should not be constrained by a binary close date. CBRE recommends a rolling tender assessed on absolute criteria: any proposal meeting the technical and financial requirements should be awarded on a first-come, first-served basis, without waiting for competing bids. This eliminates the void risk of a round attracting zero qualifying bids, removes speculative gaming, and sends a consistent pipeline signal. For a long-duration programme like the Northern Metropolis, certainty of award is worth more than price competition alone. -

Enhance Land-Use Flexibility

The current model transfers all risk to the private sector while prescribing all uses. Non-contiguous sites with rigid, government-designed allocations, residential here, E&T there, separated by geography and tenure, prevent developers from integrating uses, sequencing construction logically, or responding to actual occupier demand. A better model defines outcomes, jobs created, industry type, public facilities delivered — and allows developers to propose the most efficient configuration within a broad policy envelope. Large-scale land realises most value when developers can integrate and optimise. The Government should define what it wants to achieve, not how every square metre should be used. -

Recalibrate GFA Minimums

The combined E&T minimum GFA across the three sites is approximately 165,000 sq.m. Even at a 60% minimum threshold, the implied scale remains very large relative to current market absorption, with Hong Kong's industrial vacancy still at elevated levels. CBRE recommends a phased GFA model: let the market set minimum first-phase thresholds at a level genuinely supportable by near-term occupier demand, with upward GFA triggers tied to demonstrated occupancy milestones. This preserves long-term policy ambition while aligning near-term supply with market reality. Flexibility on GFA is not a concession. It is the difference between a built, occupied district and a failed tender. -

Modernise Building Code for Future City

The Northern Metropolis is planned as Hong Kong's next-generation urban centre, yet its new developments are governed by a building code designed for a different era, and this directly prevents the most in-demand occupiers from committing.

Logistics operators need low-rise, high-ceiling buildings with internal clearance exceeding 10 metres for modern racking and automation. AI data centres require floor-to-floor heights above 6 metres for high-density server racks and cooling infrastructure. Both are precisely the occupier types the Northern Metropolis should be attracting — yet both trigger "double GFA counting" disadvantages under the current Buildings Ordinance, making efficient industrial design financially irrational. A developer who builds to operational specification is penalised against maximum permissible GFA.

Despite the latest Q&A response issued on 29 June 2026, in which the Government stated that “...for purchasers of the Enterprises and Technology Park (E&TP) sites... the BD is prepared to accept proposals incorporating high-headroom designs in this tender without counting each high-headroom area as more than one storey in the GFA calculation,” this clarification effectively grants an exemption from the prevailing GFA controls. However, the announcement was made at a very late stage of the tender process.

GFA controls are a legitimate planning tool, but they were calibrated for residential towers and commercial offices, not precision industrial facilities with fundamentally different spatial requirements. CBRE recommends a NM-specific building code schedule exempting qualifying industrial uses from double GFA counting up to defined operational thresholds. For the first two to three decades while NM towns are being established, the priority must be attracting real occupiers with buildings that actually work, not maximising plot ratios that no one will bid for.