Valuer Insights

Business Insights | Falling Home Prices Open Doors for Homebuyers

August 28, 2025

Contact

Angus Luk

Senior Director, Valuation & Advisory Services, Hong Kong

Despite a roughly 27% decline in Hong Kong property prices from their peak, the city has still been ranked as one of the world’s least affordable housing markets for the 15th consecutive year. However, a closer look at market dynamics reveals that housing affordability has significantly improved compared to peak levels, suggesting that Hong Kong’s property market is gradually regaining its appeal.

Source: Demographia

To better understand the trend, we selected two representative transactions and analyzed current market valuations using data from the Land Registry. Mortgage affordability ratios were simulated under different interest rate scenarios, assuming a 70% loan-to-value ratio over a 30-year term. The interest rates used include the 2021 peak (1.44%), the current level (3.5%), and a projected post-rate-cut level in September (3.25%). Based on the median monthly income of two-person and four-person households, the mortgage burden ratios were calculated to reflect actual affordability.

Source: CSD

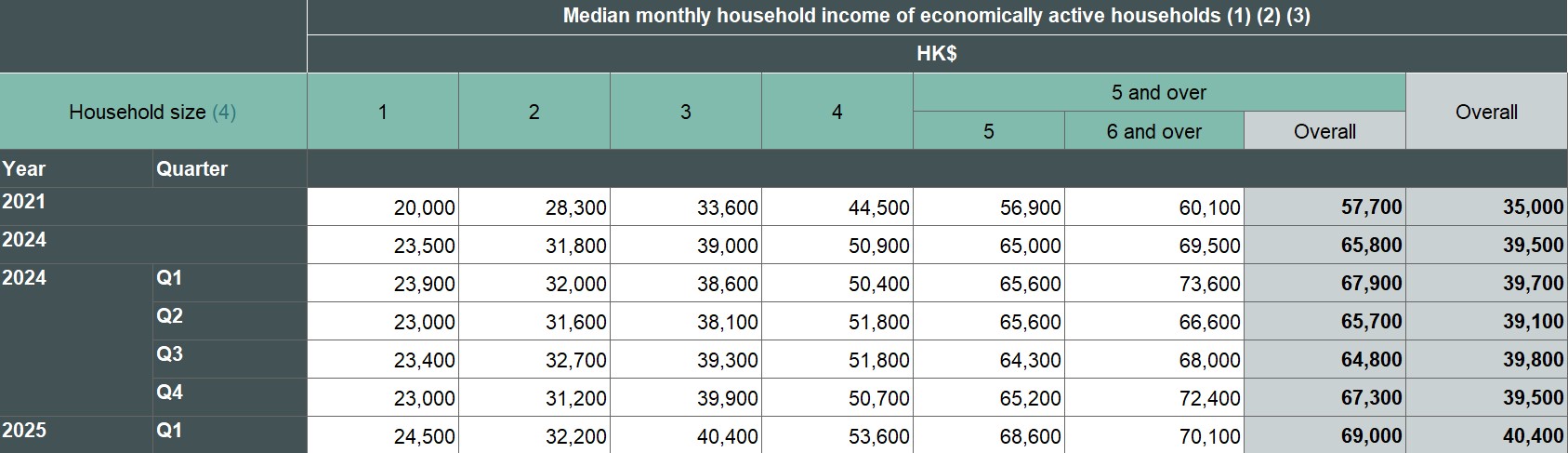

In February2021, a unit of Block 49 in City One Shatin was transacted for HK$5.9 million, with a saleable area of 285 sq. ft. Using the 2021 interest rate cap of 1.44% and a 30-year mortgage at 70% LTV, the mortgage affordability ratio was 49.9% when calculated using a two-household median income of HK$28,300.

Today, with property prices approximately 24.9% lower than their peak, reaching HK$4.43 million (based on HSBC-eval data), and the median monthly income of households residing in private properties in the first quarter of this year increasing by approximately 13.8% to HK$32,200 compared to the last quarter of 2021, the affordability picture has brightened. The current mortgage affordability ratio has fallen below 50%, reaching 43.2% in July, a decrease of approximately 13.4% compared to the 2021 peak.

In March 2021, a unit of Block 5, Chestwood Court in Kingswood Villas, was sold for HK$7.2 million (557 sq. ft.). Using the 2021 interest rate cap of 1.44%, a 30-year mortgage at 70% LTV, and a four-household median income of HK$44,500, the affordability ratio stood at 38.8%.

Considering the current context, with prices approximately 36.1% lower than their peak, now at HK$4.6 million (HSBC-eval reference), and a 20.4% increase in median monthly income for households in private properties in the first quarter of this year compared to the last quarter of 2021, the affordability ratio has significantly improved. It currently stands at 27% in July, a decrease of approximately 30.4% compared to the 2021 peak.

The data clearly shows that the barriers to homeownership have significantly lowered, with improved affordability injecting positive momentum into the property market.

Beyond improved affordability, the Hong Kong property market benefits from a wealth of available capital. Recent data from the Hong Kong Monetary Authority (HKMA) paints a picture of shifting investment strategies. While time deposits saw a dip of approximately 3.6% in June, totalling HK$10.13 trillion compared to the April peak of HK$10.51 trillion, the overall deposit base in Hong Kong remains robust.

Interestingly, current and savings deposits surged, reaching approximately HK$8.54 trillion in June – a significant jump of about 13.2%, or roughly HK$1 trillion, compared to April. This suggests a strategic reallocation of funds by investors, potentially in anticipation of more attractive investment opportunities.

The potential impact on the property market is significant. If just 1% of the existing approximately HK$10 trillion in time deposits were to find its way into real estate, it would translate to a staggering HK$100 billion in transaction volume. Based on an average unit price of HK$8 million, this influx of capital could represent approximately 12,500 potential new demands.

The confluence of favourable market conditions is likely to further strengthen buyer confidence. The growing likelihood of an interest rate cut by the U.S. Federal Reserve later this year could prompt similar moves by the Hong Kong Monetary Authority, potentially drawing additional capital into the property market.

Furthermore, the widening gap between mortgage payments and rental costs, where buying is increasingly cheaper than renting, is becoming a compelling advantage. This dynamic is not only encouraging homeownership but also reigniting investor interest, setting the stage for sustained upward momentum in both property prices and transaction volumes in the second half of the year.

Source: Demographia

To better understand the trend, we selected two representative transactions and analyzed current market valuations using data from the Land Registry. Mortgage affordability ratios were simulated under different interest rate scenarios, assuming a 70% loan-to-value ratio over a 30-year term. The interest rates used include the 2021 peak (1.44%), the current level (3.5%), and a projected post-rate-cut level in September (3.25%). Based on the median monthly income of two-person and four-person households, the mortgage burden ratios were calculated to reflect actual affordability.

Median Monthly Household Income of Economically Active Households by Household Size

Source: CSD

Case Study 1: City One Shatin

In February2021, a unit of Block 49 in City One Shatin was transacted for HK$5.9 million, with a saleable area of 285 sq. ft. Using the 2021 interest rate cap of 1.44% and a 30-year mortgage at 70% LTV, the mortgage affordability ratio was 49.9% when calculated using a two-household median income of HK$28,300.

Today, with property prices approximately 24.9% lower than their peak, reaching HK$4.43 million (based on HSBC-eval data), and the median monthly income of households residing in private properties in the first quarter of this year increasing by approximately 13.8% to HK$32,200 compared to the last quarter of 2021, the affordability picture has brightened. The current mortgage affordability ratio has fallen below 50%, reaching 43.2% in July, a decrease of approximately 13.4% compared to the 2021 peak.

Case Study 2: Kingswood Villas

In March 2021, a unit of Block 5, Chestwood Court in Kingswood Villas, was sold for HK$7.2 million (557 sq. ft.). Using the 2021 interest rate cap of 1.44%, a 30-year mortgage at 70% LTV, and a four-household median income of HK$44,500, the affordability ratio stood at 38.8%.

Considering the current context, with prices approximately 36.1% lower than their peak, now at HK$4.6 million (HSBC-eval reference), and a 20.4% increase in median monthly income for households in private properties in the first quarter of this year compared to the last quarter of 2021, the affordability ratio has significantly improved. It currently stands at 27% in July, a decrease of approximately 30.4% compared to the 2021 peak.

The data clearly shows that the barriers to homeownership have significantly lowered, with improved affordability injecting positive momentum into the property market.

Adequate Capital to Support Property Market

Beyond improved affordability, the Hong Kong property market benefits from a wealth of available capital. Recent data from the Hong Kong Monetary Authority (HKMA) paints a picture of shifting investment strategies. While time deposits saw a dip of approximately 3.6% in June, totalling HK$10.13 trillion compared to the April peak of HK$10.51 trillion, the overall deposit base in Hong Kong remains robust.

Interestingly, current and savings deposits surged, reaching approximately HK$8.54 trillion in June – a significant jump of about 13.2%, or roughly HK$1 trillion, compared to April. This suggests a strategic reallocation of funds by investors, potentially in anticipation of more attractive investment opportunities.

The potential impact on the property market is significant. If just 1% of the existing approximately HK$10 trillion in time deposits were to find its way into real estate, it would translate to a staggering HK$100 billion in transaction volume. Based on an average unit price of HK$8 million, this influx of capital could represent approximately 12,500 potential new demands.

Stronger Momentum in H2

The confluence of favourable market conditions is likely to further strengthen buyer confidence. The growing likelihood of an interest rate cut by the U.S. Federal Reserve later this year could prompt similar moves by the Hong Kong Monetary Authority, potentially drawing additional capital into the property market.

Furthermore, the widening gap between mortgage payments and rental costs, where buying is increasingly cheaper than renting, is becoming a compelling advantage. This dynamic is not only encouraging homeownership but also reigniting investor interest, setting the stage for sustained upward momentum in both property prices and transaction volumes in the second half of the year.